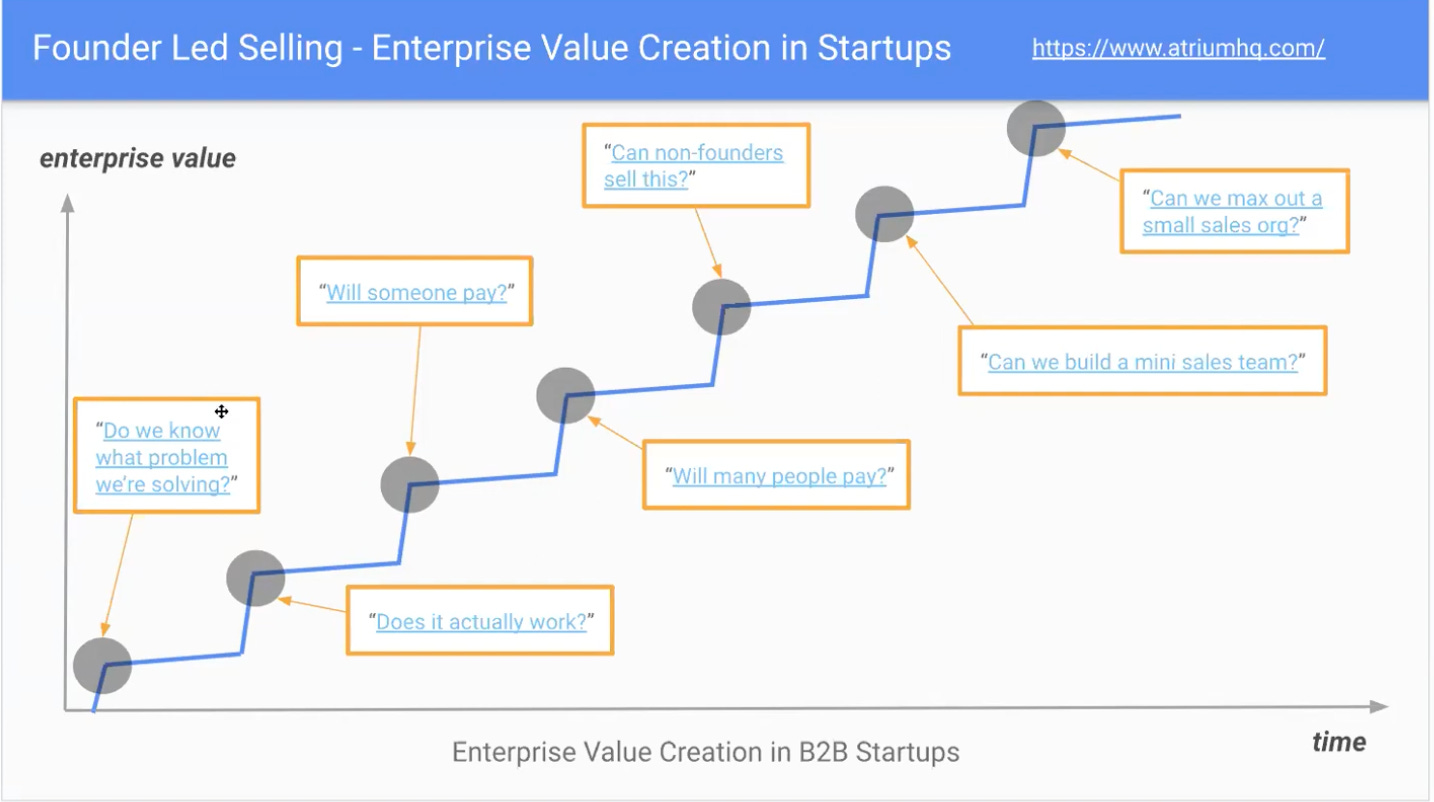

Revenue quality at pre-seed

and the can of worms early traction opens up

Occasionally, I see pre-seed companies with incredible traction. Seed stage revenue, pre-seed valuations. Sign of the times, perhaps.

These companies may seem compelling at a glance. Where I’ve been burned as an 👼🏽 and a VC is when I’ve failed to ask:

is it in the bank?

is it recurring?

is it from new/existing customers?

🏦 Is it in the bank?

There’s a big difference between a non-binding LOI and wired revenue. LOIs with a trigger clause for conversion can be a strong signal, but VCs who focus on traction really want to see recognized revenue.

That said, not all LOIs are the same.

An LOI signed 2 months ago on track to be converted into a contract in the next 1-3 months is a much stronger signal than one signed 12+ months ago. Pilots are similar; is there a clear conversion path from pilot to paid/recurring or are they dragging on because the roadmap has been delayed, the customer isn’t getting enough usage/value, or the relationship isn’t managed well.

Time kills deals. If the problem is painful enough, there’s often a short window between when a customer gets to you with a problem to solve and either activating or finding a solution elsewhere.

It’s common not to want to charge until a product is built, but if you’re working with design partners and manually handling a workflow as you build, there’s an opportunity to monetize.

🔁 Is it recurring?

Monetizing manual workflows is how startups begin to get enough revenue to build out technology to support manual or semi-automated processes. This often creates a second-order problem; making the leap from one-time to recurring revenue.

I joined my 2nd SaaS startup when we were still in the Service as a Software Flinstoning phase. A lot of our revenue was event or project-based. Revenue was lumpy and there was more overhead involved with the need to resell the customer after every project.

Luckily, this problem helped us realize that we were targeting a customer without a frequent or in turn painful enough job to be done, helping us find a more ideal customer in enterprise recruitment marketing teams, build the product out for them and create a pricing model that made the value creation:value extraction make sense.

To be clear, any recognized revenue is winning. Customers are willing to pay! But the next question is how to make that repeatable so you don’t have to burn cash on sales/success teams living life on a hamster wheel. And I now ask: is it monthly revenue or monthly recurring revenue?

💸 Is it from new or existing customers?

While hockey stick growth may be the long term goal, seeing it early makes me curious about retention. It’s hard to recover from bad initial product experiences.

I’ve seen this from two perspectives.

In one case, a company initiated 40 pilots over the course of 12 months. They signed >$300k in LOIs! But:

onboarding wasn’t figured out to get those customers to adopt

the product was tough for customers to use creating issues for even the most determined users

and while there were consistent drops of revenue with initial pilot fees, those pilots didn’t convert into paying customers

The flip is a company that has slow played growth. After closing ~$100k in ARR within the first month of launch and getting a lot of inbound interest, they paused on launching with new customers and:

hunkered down with their 5 initial pilot customers

built out launch plans for each company to roll out methodically

worked hands-on with each customer and user type to figure out what would drive adoption across each stakeholder / business type

updated their roadmap based on learnings from discovery and insight from behavioral product advisors

Should I raise on traction or vision?

As hilariously early investors at Hustle Fund, we maintain that traction doesn’t matter. A great idea pre-revenue at the right entry price is often more appealing than a company already making $250k ARR raising at a 40x revenue:valuation multiple, especially if there are problematic answers to any of the above.

While early traction can be a great signal, it often provides a pandora’s box for VCs to poke at. In addition to the above, velocity of growth, customer concentration and more can/will be challenged. And at pre-seed, priority #1 is knowing what problem you’re solving. GTM legend Pete Kazanjy, author of Founding Sales shared more in a recent conversation with Elizabeth Yin.

To be clear, I’m not making a case against early revenue, moreso a note on what happens once you focus on traction vs. the problem you’re solving. And I believe that more founders who have learned from the frothiness of 2020 2021 will wait to raise until they’ve validated the problem, built an MVP, and recognized revenue from recurring, retentive customers to have more control over their destiny.

More of what we do look for in early stage startups here.

Resources

You earn a million dollars a year and can’t get funded? - David Frankel, Founders Collective

All revenue is not created equal - Bill Gurley, Benchmark